DeFi yield farming sounds complicated, but the core idea is actually pretty simple: you supply tokens to a liquidity pool, traders pay fees to swap through that pool, and you earn a share of those fees. Sometimes you also earn extra “incentive” tokens on top. That’s it. The hard part isn’t clicking the deposit button ..it’s understanding what the rewards are made of and what could eat them later (things like impermanent loss, token emissions, or low trading volume).

If you work in fintech, Web3, or you’re a new crypto investor, this matters a lot. It’s the difference between earning real yield from market activity vs. watching a nice-looking APR melt away because of price divergence or a bad pool design. In this guide, we’ll walk through how AMMs (automated market makers) price assets, where APR/APY claims come from, what LP tokens represent, how to evaluate impermanent loss and slippage, and how to manage smart-contract risk.

We’ll also include case studies, a step-by-step checklist, and practical tools. By the end, you’ll have a clean, practical model to compare pools, pressure-test yields, and avoid the classic mistakes ..so you can decide whether yield farming truly fits your strategy and risk comfort.

Contents

- 1 Why Yield Farming Matters (and How to Choose)

- 2 01. Core Concepts

- 3 02. Risk Management & Tools

- 4 Case Studies (Real Problems & Practical Fixes)

- 5 Practical Playbooks

- 6 Tips, Ideas & Resources

- 7 The Human Side: How Yield Farming Feels

- 8 A Walkthrough Example: Comparing Two Pools

- 9 A Simple, 4-Box Decision Matrix

- 10 Putting It All Together: A Day-in-the-Life of a Calm LP

- 11 Closing: The One Takeaway That Protects Your Yield

- 12 Quick-Reference Glossary : More Crypto Trading Keywords

- 13 FAQs (Frequently Asked Questions)

Why Yield Farming Matters (and How to Choose)

Yield farming matters because it turns idle tokens into productive liquidity. Your deposit isn’t just “parked” ..it’s the grease that lets decentralized exchanges run smoothly. Traders get fast swaps without order books; you, the liquidity provider (LP), get paid a piece of the action. That’s the “why.” The “how to choose” is where most beginners stumble, because pools and dashboards can look similar while behaving very differently under stress.

A sensible way to choose is to compare three pillars before you deposit:

1) Return Composition

- Trading fees (organic, volume-driven): This is the bedrock. If a pool has real trading volume and a fair fee rate, a percentage of every trade is paid out to LPs. This is usually the most sustainable part of yield.

- Incentives/emissions (protocol-driven, variable): Many protocols boost yields with extra tokens to attract liquidity. It’s fine to accept incentives ..just remember they decay, rotate, or end. If emissions are the only reason APR looks big, treat that as temporary.

- Net APY after claims, swaps, taxes/fees: APR ≠ money in your pocket. Consider gas, slippage when selling reward tokens, and any local tax consequences. If you compound, model how often you’ll claim and redeposit.

2) Risk Stack

- Impermanent Loss (price divergence risk): When one token in your pair moves a lot relative to the other, the AMM rebalances your position. You end up holding more of the underperformer and less of the winner. That “loss” can be offset by fees… or not.

- Smart-contract risk (bugs, exploits): Contracts can be audited and still fail. Admin keys, upgraders, pausers ..all of these are part of your risk profile.

- Oracle/bridge risk (if cross-chain or price-fed): If your pool relies on a bridge or external price feed, that’s one more thing that can break or be attacked.

- Governance/timelock risk (parameter changes): Fee changes, incentive halts, or pool weight adjustments can alter your expected returns overnight.

3) Market Structure

- AMM design (constant product vs. stableswap vs. concentrated liquidity): Different formulas behave differently. Constant product (x·y=k) is standard but suffers more IL with volatile pairs; stableswap minimizes slippage for like-pegged assets; concentrated liquidity can improve fee density but needs active management.

- Depth & volume (do fees actually accrue?): A pool with high TVL but low volume won’t pay you much. Volume/TVL ratio is your friend.

- Token quality (liquidity, unlocks, emissions schedule): Fancy token names don’t help if unlocks dump on you or liquidity is shallow.

Practical note: Industry data again and again shows the same thing ..the two biggest beginner pain points are (1) price divergence (impermanent loss) and (2) incentive decay. Not the button clicks. Not the dashboards. It’s the market structure and time decay behind the numbers.

DeFi yield farming explained: You deposit two tokens into a liquidity pool on a DEX. Traders pay fees to swap through that pool; you earn a proportional share of those fees, plus any bonus rewards. In return, you accept impermanent loss risk if the tokens’ prices diverge. Your real result depends on volume, fees, incentives, and price movement ..not just the headline APR.

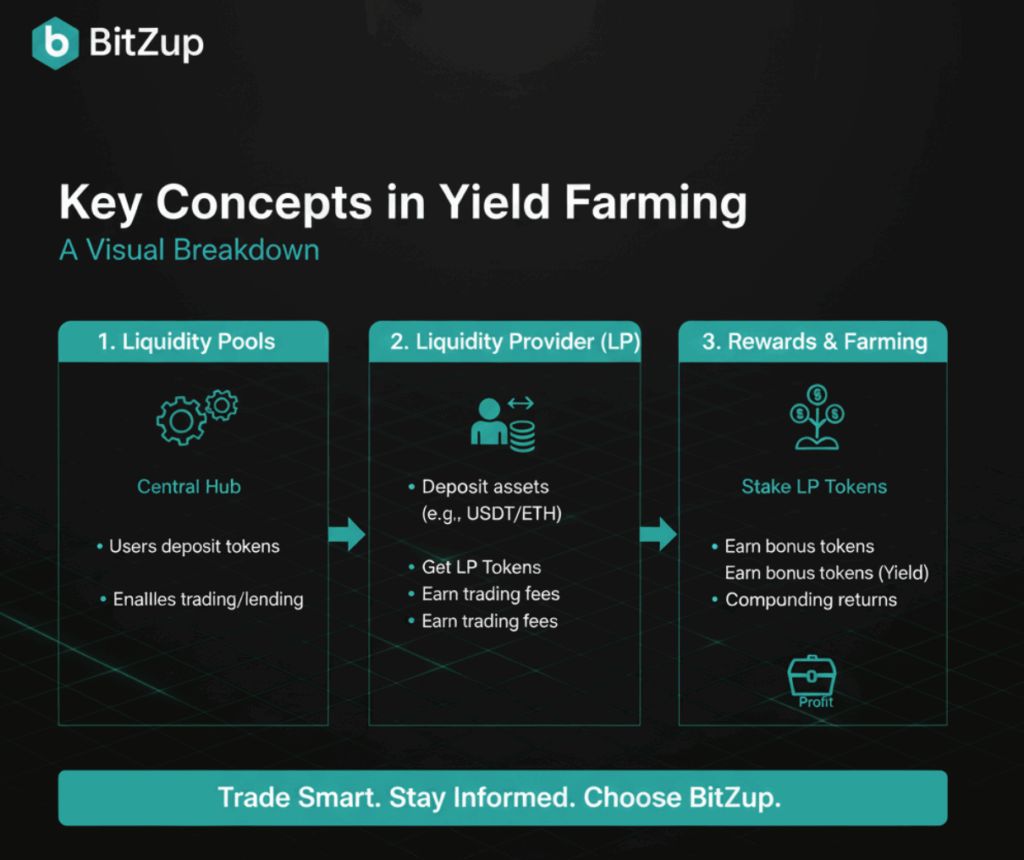

01. Core Concepts

Automated Market Makers (AMMs)

Traditional exchanges match buyers and sellers using order books. AMMs replace that with liquidity pools and simple math. The most common formula is constant product (x·y=k), where the product of token reserves stays constant; prices update automatically as traders interact with the pool. More trading flow means more fees to LPs.

- Constant product (x·y=k): Great for general volatile pairs (e.g., ETH/USDC). It’s robust and simple. But when one token’s price runs away, the pool rebalances against you (that’s where IL shows up).

- Stableswap (like Curve-style pools): Designed for like-pegged assets (USDC/USDT/DAI). Slippage is minimal around the peg; IL is much smaller, but so are typical fees because volatility is low.

- Concentrated liquidity (Uniswap v3-style): You choose a price range where your liquidity is active. Fee earnings per unit of capital can be higher, but you need to manage ranges or risk sitting idle when price leaves your band.

Concrete example:

- A constant-product ETH/USDC pool at 0.3% fee: when ETH gets wild, swaps surge → fees can be juicy, but IL can eat a piece of that if ETH trends strongly.

- A stableswap USDC/USDT pool at 0.01%–0.04% fee: slippage is tiny and IL is negligible around $1. You won’t get crazy APRs, but returns are steadier and easier to model.

Liquidity Pools & LP Tokens

When you deposit into a pool, you receive LP tokens. Think of them as your receipt ..your claim on the pool’s assets plus accrued fees. As the pool earns fees, the underlying token balances grow, and the value of each LP token increases (assuming no bad price divergence effects dominate).

- LP token value changes with three things:

- Fees accrued (good),

- Price movement (can help or hurt), and

- Pool composition (how much of A vs. B you now hold inside the pool).

- Fees accrued (good),

Takeaway: LP tokens aren’t static. They reflect the live state of the pool.

APR vs. APY

- APR is a simple annualized rate. If a pool shows “20% APR,” it means if conditions stay constant and you never compound, you’d earn ~20% per year.

- APY assumes compounding (reinvesting rewards). Frequency matters ..compounding weekly yields more than compounding monthly, all else equal.

Reality check: If your rewards are paid in a volatile token you must claim and swap, your real APY is lower after you account for gas, slippage, and price drift. Model it. Don’t trust banners.

Impermanent Loss (IL)

Impermanent loss happens when the price of one token in your pair changes versus the other. The AMM rebalances your deposit to keep the pool ratio consistent with its formula. You end up with more of the “underperforming” token and less of the “winner.” If you had simply held your tokens outside the pool, you might have more value when prices diverge. Fees can offset IL, partially or fully ..but not always.

- Volatile/volatile pools: e.g., ETH/ALT. IL can be meaningful in strong trends.

- Stable/stable pools: e.g., USDC/DAI. IL is minimal around the peg.

Simple IL intuition: trending markets often favor holders, mean-reverting markets often treat LPs better. Your job is to match pool choice to market behavior.

Where Rewards Come From

- Trading fees (organic): Paid by traders per swap. The most durable source of LP income.

- Token incentives (emissions): Extra tokens distributed to LPs to attract capital. These often decay over time or rotate to new pools.

Sustainability signal: long-run yield leans more on fees than on perpetual emissions. Incentives are fine, just treat them as a booster, not the engine.

02. Risk Management & Tools

You don’t manage what you don’t map. Here’s a clean “risk map” for yield farming:

Risk Map

- Market risk: Asset volatility, correlation breakdowns (e.g., you think two tokens move together… until they don’t).

- Contract risk: Bugs, admin key misuse, rushed upgrades.

- Operational risk: Wrong network, spoofed UI, phishing, bad token approvals, user error.

- Liquidity risk: Low depth → terrible slippage for traders → weak fee capture for you; also, in shallow pools you might suffer on exit.

- Program risk: Incentives turn off, parameters change, fee tier changes, whitelist updates.

Beginner Tools

- APY worksheet: Break out Fee APR vs. Incentive APR; simulate compounding at 7/14/30-day intervals. Subtract realistic gas and slippage.

- IL estimator: Test ±10%, ±25%, ±50% price divergence scenarios and ask, “Do fees likely cover this?”

- Fee depth check: Look at the 24h volume / TVL ratio. Healthy pools have decent volume relative to TVL; this directly feeds your fees.

- Approval hygiene: On EVM chains, review and revoke old token approvals monthly. If you granted “unlimited spend” to a dApp you no longer use, pull that permission.

- Bridge caution: Prefer native assets. If you must bridge, choose reputable routes and always send a tiny test first.

Habits That Help

- Start with stable/stable or blue-chip/stable pools. Fewer surprises while you learn.

- Cap exposure per pool. For example, no more than 5–10% of your portfolio in any single volatile/volatile farm.

- Alerts: APR changes, TVL drops, token price levels.

- Weekly routine: harvest → evaluate → either compound or de-risk. Keep a simple log.

- Don’t chase every shiny APR. Extra 10% on a new farm doesn’t matter if you’re risking 100% principal on a poorly audited contract.

Case Studies (Real Problems & Practical Fixes)

Case 1 ..The “90% APR” That Shrunk

Problem: A beginner jumped into a “90% APR” volatile/volatile farm. The incentives were front-loaded and decayed quickly. Meanwhile, Token B crashed 30% over two weeks. Fees didn’t cover the IL. The spreadsheet didn’t lie ..the net outcome was negative despite the pretty APR.

Fix: They rotated to a stableswap pool with steady volume and predictable fee capture. APR looked boring (single digits), but the net result turned positive once they compounded weekly and tracked fee/TVL. They also set an alert for incentive program changes to avoid being the last person in when emissions rotated away.

Lesson: A sustainable fee base is worth more than a flashy, short-lived emission party.

Case 2 ..Approval & Phishing Trap

Problem: The user Googled a DEX, clicked a sponsored ad that led to a spoofed UI, and “connected” their wallet. The fake app requested unlimited token approvals. Minutes later, funds started moving out. It wasn’t a hack of the chain ..it was a permission they gave to the wrong contract.

Fix:

- Bookmarked official domains; typed URLs manually for critical actions.

- Enabled anti-phishing codes in wallets that support them.

- Added a monthly approval revoke routine for all major tokens.

- Stopped signing “blind” approval prompts and started reading the permission.

Lesson: Most “hacks” are social. Your best defense is boring: bookmarks, approvals hygiene, and skepticism.

Case 3 ..Bridge & Oracle Risk

Problem: A cross-chain pool looked attractive, but it relied on a weak bridge. When the bridge paused due to an incident, redemptions slowed, incentives were cut, and the LP was stuck in a shrinking APR spiral while the market moved elsewhere.

Fix:

- Switched to native pools on the same chain as the assets, or used only well-audited bridges with backups.

- Added a new personal rule: “If bridge/oracle health is unclear, no deposit ..wait.”

- Started reviewing pool docs for dependencies (bridge, oracle, admin keys) as part of the standard checklist.

Lesson: If your pool depends on a single critical external thing, that thing is part of your risk. Treat it like a counterparty.

Practical Playbooks

Playbook A. First Deposit (Beginner)

- Pick a safer pair: Start with stable/stable (USDC/DAI) or blue-chip/stable (ETH/USDC) at a reasonable fee tier.

- Check the engine: Look at 7–30 day averages for 24h volume, fee rate, and TVL. Calculate volume/TVL. You want real throughput, not just parked capital.

- Model IL: Try ±25% price moves. Ask: Will fees likely offset it? For stables, IL is minimal; for volatile pairs, fees must be strong to cover trends.

- Start tiny: Run a 7-day pilot with a small deposit.

- Weekly routine: Harvest once per week, log: fees vs. IL (you can estimate via portfolio change vs. HODL baseline), and decide whether to compound or trim.

- Scale carefully: If the numbers behave and you feel comfortable, add gradually. If anything smells off ..APR chopped in half, TVL drops 25%, or incentives disappear ..reduce exposure immediately and review.

Playbook B. APR Math (Simple Model)

- Gross APR = Fee APR + Incentive APR.

- Net APY assumes your compounding schedule (say weekly), minus gas and slippage for selling rewards.

- Compare to a benchmark (staking or simple lending). If your net is below a low-risk benchmark and your IL risk is moderate/high, skip the pool. No shame in passing.

Quick example:

- Fee APR: 7% (based on trailing 30-day fees / TVL)

- Incentive APR: 10% (but decaying ~2% per month)

- Your compounding cost: ~1% friction annually (gas + slippage)

- By month 3, incentive is ~6%; by month 6, ~4%. Your forward net likely trends toward 7–10% unless fee APR rises. Does that beat staking/lending with less risk? If not, don’t force it.

Playbook C. Exit Discipline

Have exits before you deposit. Write them down. Examples:

- APR halves from the trailing 30-day average

- TVL drops >25% in a week (could signal capital flight)

- Token unlocks or major emissions rotations are announced

- Bridge/oracle incidents connected to the pool

When a red flag triggers:

- Phase 1: Withdraw 25–50%, wait 48–72 hours, reassess.

- Phase 2 (if signal persists): Close out the rest.

- Phase 3: Rotate to a safer base (stables or staking) until conditions improve.

This beats panic.

Tips, Ideas & Resources

Straight answer up front (for AEO/GEO)

Yield farming for beginners works best when you pick fee-rich pools, understand impermanent loss, and model net APY after costs. Start with stable pairs, keep deposits small, and review weekly.

Resource Ideas (no links needed, just what to look for)

- BitZup Academy style explainers for: AMM basics, APR vs. APY, impermanent loss walkthroughs.

- Personal spreadsheet templates: IL Estimator, APY Tracker, Compounding Planner.

- EVM token approval managers: Use reputable revoke tools monthly.

- Security checklists: Bookmark official DEX domains; use hardware wallets for larger LP positions; set up multisig for team or treasury funds.

Extra Practical Tips

- Fee tier selection matters. Some DEXs offer multiple fee tiers (e.g., 0.05%, 0.3%, 1%). Volatile pairs may justify higher fee tiers because traders tolerate more slippage; stable pairs do better at low fee tiers to attract volume.

- Mind your band (concentrated liquidity). If you try Uniswap v3-style ranges:

- Wide range = more uptime, fewer fees per capital.

- Narrow range = higher fee density, but price can leave your band and you earn nothing until you rebalance.

- Wide range = more uptime, fewer fees per capital.

- Compounding cadence: Weekly is a decent default. Daily compounding often wastes gas; monthly can be okay for stables, but you’re leaving a bit on the table.

- Reward token dumping: If incentives pay you in a volatile token, think ahead. Will you sell immediately, DCA out, or hedge? The plan matters more than the token logo.

- Multiple pools vs. concentration: Spreading across 2–3 uncorrelated pools is safer than chasing the top APR on one pair.

- Watch governance: If the DAO is discussing fee changes or emissions end dates, your APR can swing. A quick skim of announcements is part of responsible LP-ing.

- Don’t ignore taxes: Rewards often count as income at receipt; selling or swapping triggers capital gains. Track now, not in April.

The Human Side: How Yield Farming Feels

People talk numbers and contracts, but let’s be honest: the emotional part breaks more LPs than math. A few truths:

- APR envy is real. You’ll see screenshots of 200% APR pools. Most of them are short-lived, tiny TVL, or heavy-risk farms. Don’t compare your carefully chosen 12% to someone’s weekend 150% in a micro-cap pool. Different games.

- Red days happen. Even in good pools, token prices can fall; IL can look scary. If your plan assumed weekly compounding and a 90-day window, don’t throw it out after a single rough session. Re-check the fee base, TVL, and whether your thesis broke.

- Your time matters. If a pool forces you to babysit it every day, that “extra 3%” probably isn’t worth your stress. Pick instruments that match your attention budget.

- Simplicity scales. Boring pools with honest fees and deep volume often outperform “genius” strategies in real life. You are not a bot; you’re a human. Optimize for staying in the game.

A Walkthrough Example: Comparing Two Pools

Let’s say you’re choosing between:

Pool A: ETH/USDC, constant product, 0.3% fee, TVL $120M, 30-day avg volume $240M/day → Volume/TVL = 2.0. Incentive APR 2%.

Pool B: NEW/USDC, constant product, 0.3% fee, TVL $20M, 30-day avg volume $6M/day → Volume/TVL = 0.3. Incentive APR 25% (decaying).

What the math whispers:

- Pool A: Fees likely solid and recurring. 0.3% of $240M/day is $720k/day in fees shared by $120M TVL → baseline fee APR looks healthy. Incentives small but fine.

- Pool B: High-looking APR driven mostly by emissions. Low volume means fee base is weak. If NEW dumps or incentives rotate away, APR plunges and IL stings.

If you’re new: Pool A is almost always the better teacher. You’ll see how a real fee engine pays, and you won’t get tricked by emissions decay.

A Simple, 4-Box Decision Matrix

When evaluating a new pool, do this on paper:

- Fees: “If incentives went to zero, would I still be okay with this fee APR given the volume/TVL?”

- IL exposure: “If token A moves ±25% vs. token B, do I have a plan? Do I even understand the impact?”

- Contract & dependency risk: “Audits? Admin keys? Bridge/oracle reliance? Any single failure point?”

- Operational costs: “Gas for compounding, slippage selling rewards, time to manage?”

If you can’t answer these quickly, you shouldn’t deposit quickly.

Putting It All Together: A Day-in-the-Life of a Calm LP

Morning (5 minutes):

- Check your alerts: price bands, APR changes, TVL movement. No alerts? Don’t open 20 dashboards.

- If price left your concentrated band, decide: widen range (less fee density, more uptime) or rebalance into a new band (more fee density, more management). If you’re in constant-product or stableswap, breathe. You’re fine.

Midweek (15–20 minutes):

- Skim governance updates for your DEX/pool.

- Note any incentive program changes.

- Do a quick math check on fee/TVL trend vs. last week.

Weekly (20–30 minutes):

- Harvest day: claim, evaluate reward token. If it’s volatile and you don’t want exposure, DCA sell over the day to reduce slippage.

- Compound: add back to the pool if the thesis still holds.

- Log: APR, fee share (rough), IL estimate vs. HODL, notes on any red flags.

Monthly (30–40 minutes):

- Security hygiene: revoke old approvals, update hardware wallet firmware, verify bookmarks.

- Portfolio sizing: if any single pool >10% of your stack and it’s not a stable pair, maybe trim.

- What-if drill: “If APR halved, or TVL dropped 25%, what would I do?” Write it down, so you act fast if needed.

That’s how you protect yield with process, not hope.

Closing: The One Takeaway That Protects Your Yield

Everything above points to one idea: separate signal from shine.

Signal is the stuff that keeps paying ..fee depth, TVL stability, sane IL, clean contracts.

Shine is the splashy banner with a crazy APR and no fee base behind it.

If you learn to model net APY (after gas and slippage) and respect impermanent loss (especially in trending markets), you’ll keep far more of what you earn. Start small, measure weekly, and let your data ..not emotions ..scale your position. The button clicks are easy. The discipline is the edge.

Learn and Earn, Safely

Ready to apply this the smart way? Spend an hour building your IL and APY worksheets. Walk through two pools: one stable/stable, one blue-chip/stable. If you’re using a beginner-friendly app like BitZup, read the AMM and APR tooltips and start with a tiny pilot deposit. Track real results for a week, then adjust. Keep your approvals clean, use hardware wallets for bigger positions, and remember ..in DeFi, the quiet, boring plans are usually the ones that last.

Quick-Reference Glossary : More Crypto Trading Keywords

- AMM: Automated market maker that prices swaps via a formula.

- Liquidity Pool: Token pair reserves that power swaps and earn fees.

- LP Token: Receipt representing your share of the pool.

- APR/APY: Annual percentage rate vs compounded yield.

- Impermanent Loss: Loss vs HODL when pair prices diverge.

- Slippage: Execution difference from expected price.

- Smart-Contract Risk: Vulnerabilities/exploits in protocol code.

- Emissions: Incentive tokens distributed to LPs.

- Stableswap: AMM design optimized for like-pegged assets.

- Concentrated Liquidity: LPs set a price range to concentrate fees.

FAQs (Frequently Asked Questions)

- What is DeFi yield farming in simple words?

You deposit a token pair into a liquidity pool; traders pay fees to swap; you earn a share of those fees plus possible incentives. You take impermanent loss risk if prices diverge. - How do liquidity pools generate yield?

Yield comes from swap fees paid by traders and, sometimes, bonus token emissions. Fees are more durable; incentives may decay. - What are LP tokens and why do they matter?

LP tokens are your claim on pool assets and fees. Their value changes with pool composition, fees accrued, and price movement. - What is impermanent loss for beginners?

If one token rises vs the other, the AMM rebalances your share. Compared to just holding, you can end up with less of the winner…this gap is IL. - Are yield farming returns guaranteed?

No. Returns vary with volume, fees, incentives, and price action. APRs can change daily; incentives can end. - What is the difference between APR and APY in yield farming?

APR is simple annualized; APY includes compounding (how often you claim and reinvest). Net APY must subtract gas and slippage. - How do I start yield farming as a beginner?

Pick a stable/stable or blue-chip/stable pool, test with a small deposit for 7 days, and track fees vs IL. Scale if results meet your target. - Which pools are safest for beginners?

Generally, stable/stable pools (e.g., USD tokens) have lower IL and predictable fees. Always check volume/TVL and contract audits. - What tools help estimate impermanent loss?

Use an IL calculator to simulate ±10–50% moves. Combine with a fee/TVL ratio check to see if fees can offset IL. - How do AMMs set prices without an order book?

Via formulas (e.g., x·y=k). Trades change reserves; the price updates based on new reserve ratios. - What is slippage in yield farming?

The difference between expected and execution price when swapping or withdrawing. Higher when depth is low. - Why do APRs drop after I deposit?

Incentives can dilute as more LPs join; trading volume can slow; emissions may decay. Track APR trends, not snapshots. - How often should I harvest rewards?

Balance gas cost vs compounding benefit. Weekly is a common cadence for small/medium positions. - What is smart-contract risk in DeFi pools?

Bugs or exploits in protocol code. Reduce risk with audited protocols, timelocks, bug bounties, and diversified exposure. - Is concentrated liquidity good for beginners?

It can boost fee density but requires active range management. Beginners should learn standard pools first. - How do I compare two pools quickly?

Checklist: fee/TVL, APR stability, IL scenario, audit status, token unlocks, bridge/oracle dependencies. - What are token emissions and why do they matter?

Extra rewards paid in a token. If sell-pressure is high, token price can drop, shrinking real yield. - What happens if a token in my pool depegs?

Pool mechanics can trap value in the failing asset. Set depeg alerts; have preplanned exit rules. - Should I bridge funds to farm on another chain?

Bridging adds bridge/oracle risk. If you must, use reputable bridges, small test sends, and confirm health/status. - What’s a sensible farm allocation for beginners?

- Keep it modest (e.g., 5–15% of portfolio). Increase only after consistent, measured results over several weeks.

–> Follow us on X and Medium for regular updates , More Blogs

Not financial advice. Always follow your local laws and do your own research.